The AI-energy trade is the group of stocks tied to powering AI data centers: nuclear and gas power producers, power-equipment makers, small modular reactor developers, and uranium suppliers. It exists because data centers are a fast-growing source of electricity demand, projected by the U.S. Department of Energy to reach 6.7% to 12% of US electricity by 2028, up from about 4.4% in 2023. This is a map of the complex, not a recommendation to buy any of it.

This content is for information and education only and is not investment advice, and it is not a recommendation of any security. Data is current as of July 3, 2026.

What is the AI-energy trade?

The AI-energy trade is the part of the AI theme that focuses on electricity rather than chips. It groups together the companies that generate, equip, and fuel the power that AI data centers consume, and it has become one of the most active corners of the market in 2026.

From chips to megawatts

The broader AI trade started with semiconductors and cloud infrastructure. As the buildout has grown, the binding constraint has shifted toward power, because data centers need enormous and reliable electricity. That shift is what pulled utilities, nuclear operators, power-equipment makers, and uranium names into the AI conversation.

A theme built on a real input

Unlike a purely sentiment-driven theme, the AI-energy trade rests on a measurable input: electricity demand. That gives it a concrete, government-sourced number at its center, which is unusual for a market theme and is where this article starts.

Why did AI become a power trade?

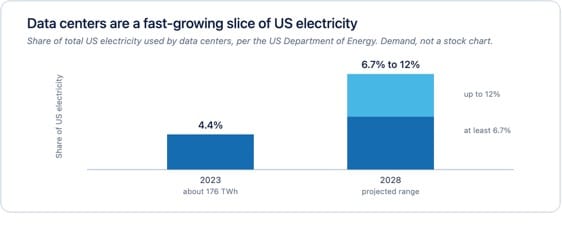

AI became a power trade because data centers are a large and fast-growing source of electricity demand. According to a U.S. Department of Energy report prepared by Lawrence Berkeley National Laboratory, data centers consumed about 4.4% of total US electricity in 2023, and are projected to consume roughly 6.7% to 12% by 2028.

US data-center electricity use, from a U.S. Department of Energy report. This is electricity demand, not a stock chart or a forecast of any stock.

The number at the center

In 2023, US data centers used about 176 terawatt-hours of electricity, or roughly 4.4% of the national total, per the Department of Energy. The same report projects that share could reach between 6.7% and 12% by 2028, a wide range that reflects genuine uncertainty about how fast the buildout continues. Either way, it is a large increase in demand over a few years, and it is the fact underneath the whole theme.

Why the number matters for traders

A projected rise in electricity demand does not tell a trader what any stock will do; it explains why the market is paying attention to power names at all. The demand figure is the theme’s fundamental anchor, and it is why utilities and nuclear operators, long treated as slow-moving, have become some of the market’s more actively traded names.

How does AI demand reach power stocks?

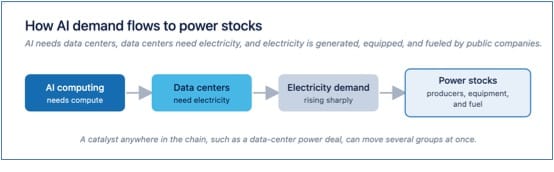

AI demand reaches power stocks through a chain: AI computing needs data centers, data centers need electricity, and that electricity is generated, equipped, and fueled by public companies. Understanding that chain is how a trader connects an AI headline to a power-stock move.

How AI demand flows to power stocks: from AI computing to data centers to the electricity they need, supplied by generators, equipment makers, and fuel producers.

The links in the chain

Each link is a different set of companies. The generators are the utilities and independent power producers, including nuclear operators. The equipment makers build the turbines and grid gear. The fuel suppliers provide uranium and other inputs. A catalyst anywhere in the chain, such as a large data-center power deal, can move names in several of these groups at once.

Why the chain trades together

Because these companies all depend on the same underlying demand, they tend to move together on shared catalysts, and a strong data-center power story can lift generators, equipment makers, and fuel names in sympathy. That connectedness is why the AI-energy names are watched as one theme rather than as separate utility stocks.

How is the AI-energy complex structured?

The AI-energy complex breaks into four segments: nuclear and gas power producers, power-equipment makers, small modular reactor developers, and uranium and fuel suppliers. Each plays a different role and carries a different financial character.

| Segment | Role in the AI-power chain | Example listed names | Financial character |

| Nuclear and gas power producers | Generate the electricity data centers buy | Constellation Energy, Vistra, Talen, NRG | Established, profitable |

| Power equipment | Builds turbines and grid gear | GE Vernova | Established, profitable |

| SMR developers | Building next-generation reactors | Oklo, NuScale, Nano Nuclear | Pre-revenue, speculative |

| Uranium and fuel | Supplies nuclear fuel | Cameco and uranium names | Cyclical, commodity-linked |

The AI-energy complex by segment. Example listed names are shown for reference only and are not recommendations.

Different roles, different risk

The segments do not behave the same way. Established producers earn revenue and profits today; SMR developers are building technology that is not yet generating power at scale. Knowing which segment a name sits in is the first step to understanding its risk, and the names above are listed as members of each segment, not as suggestions to trade.

Profitable producers vs pre-revenue developers

The most important distinction in the AI-energy complex is between established, profitable power producers and pre-revenue small modular reactor developers. They are grouped together in headlines but are very different in financial reality and in risk.

The AI-energy complex splits into established, profitable producers and pre-revenue developers building technology that is not yet generating power at scale.

What the estimates show

The difference shows up plainly in earnings estimates. For the season ahead, the established producers carry positive consensus earnings estimates: Constellation Energy, Vistra, Talen, NRG, and the equipment maker GE Vernova are all expected to report profits. The SMR developers, by contrast, carry negative estimates: Oklo, NuScale, and Nano Nuclear are expected to report losses, because they are pre-revenue companies building for the future.

Why the split matters

An established producer is valued on the power it sells now; a pre-revenue developer is valued on what it might build later, which makes it far more speculative and volatile. Treating the two as interchangeable is a common mistake, and the split is one of the most useful things to understand before following any name in this theme. This is a risk distinction, not a recommendation to favor either group.

The role of power-purchase agreements

Power-purchase agreements, or PPAs, are long-term contracts in which a large electricity buyer agrees to purchase power from a producer, and they have become a key catalyst in the AI-energy trade. When a hyperscaler signs a PPA with a nuclear operator, it can move the producer’s stock.

Why PPAs move stocks

A large, long-term power contract gives a producer revenue visibility, which is why these deals are watched closely. As widely reported, technology companies have signed power agreements with nuclear and other producers to secure electricity for data centers. These deals are covered as catalysts; the specifics of any deal should be confirmed against the companies’ own announcements, and this article does not assess any particular deal.

The reporting, attributed

Coverage of the AI-power link runs regularly in the financial press. In early July 2026, CNBC reported on GE Vernova as one company benefiting from the AI boom through its power business, an example of how equipment and power names are being tied to AI demand. Such headlines are context, not signals, and they are attributed here to their outlets.

What could slow the AI-energy trade?

The AI-energy trade rests on projections, and several things could slow it: the demand ramp could come in lower than expected, efficiency gains could reduce power needs, and grid, permitting, and policy constraints could delay projects. These are the reasons the theme carries real two-way risk.

The demand range is wide

The Department of Energy’s own projection is a range, from 6.7% to 12% of US electricity by 2028, and that width reflects genuine uncertainty. If the AI buildout slows, or if data centers become more energy-efficient, demand could land at the lower end, which would weaken the fundamental case that supports the theme. A projection is not a promise.

Bottlenecks and policy

Building new power generation, especially nuclear, takes years and faces permitting, regulatory, and financing hurdles. The pre-revenue developers in particular depend on licensing and construction milestones that can slip. Grid constraints can also limit how quickly new demand is met. These are the practical brakes on a theme that headlines sometimes treat as a straight line.

The same sustainability debate

The AI-energy trade is tied to the broader debate over whether AI capital spending is sustainable, the same debate that runs through the wider AI theme. If the market cools on AI infrastructure spending, the power names that depend on it can cool too. Credible analysts argue both sides, and this article takes no position on how it resolves.

How does the AI-energy complex trade?

The AI-energy complex trades with high correlation on shared catalysts and with wide differences in volatility between its segments. Established producers move more like utilities with an AI overlay; the SMR developers move like speculative growth stocks.

Correlation and sympathy

A major data-center power deal or a strong result from one large producer can move the group in sympathy, even before other names report. The theme rises and falls together on the big demand-side catalysts, which is why traders watch the whole complex rather than a single name.

Very different volatility

Within the theme, volatility varies widely. A large, profitable producer tends to move in smaller percentages; a pre-revenue developer can swing sharply on news, funding, or sentiment. That range is why position sizing and risk controls matter, and why leverage, which amplifies both gains and losses, is especially risky on the speculative names.

The catalyst calendar traders track

The catalysts that move the AI-energy complex are mostly earnings and power deals, and the earnings dates are on the calendar. The table below shows the confirmed dates and consensus estimates for a set of AI-energy names this season.

| Company | Segment | Report date | EPS est. |

| GE Vernova (GEV) | Power equipment | Jul 22, 2026 | 3.14 |

| Constellation Energy (CEG) | Nuclear producer | Jul 30, 2026 | 2.53 |

| Cameco (CCJ) | Uranium | Jul 31, 2026 | 0.38 |

| NRG Energy (NRG) | Power producer | Aug 4, 2026 | 1.77 |

| Vistra (VST) | Power producer | Aug 5, 2026 | 2.06 |

| Talen Energy (TLN) | Power producer | Aug 5, 2026 | 3.53 |

| NuScale Power (SMR) | SMR developer | Aug 5, 2026 | -0.13 |

| Oklo (OKLO) | SMR developer | Aug 10, 2026 | -0.17 |

| Nano Nuclear (NNE) | SMR developer | Aug 12, 2026 | -0.27 |

AI-energy earnings catalyst calendar with consensus EPS estimates. Source: Finnhub, retrieved 2026-07-03. Confirm before each event.

The estimates themselves carry the theme’s main lesson: the established producers are expected to report profits, and the SMR developers to report losses. How each stock moves on its report depends on the surprise versus expectations, a mechanic our Knowledge Hub covers.

Recent developments

Recent coverage keeps tying power and nuclear names to AI demand, and it runs alongside the debate about whether the buildout is sustainable. The items below are dated reporting, attributed to their outlets, and are context rather than signals.

- In early July 2026, CNBC covered GE Vernova as benefiting from the AI boom through its power business.

- The same DOE analysis behind this article’s demand figures reflects the official view that data-center electricity use is set to rise substantially through 2028.

These are examples of how the theme is being covered and studied, not endorsements of any view or any stock. Coverage changes constantly, and this section is refreshed as the theme develops.

What are the risks?

The AI-energy trade carries speculative-developer risk, concentration risk, commodity risk, and policy risk, and leverage magnifies all of them. The pre-revenue SMR names in particular are high-risk, and the demand projections that anchor the theme are estimates, not certainties.

- Speculative developers: pre-revenue SMR names can move sharply and can fall as fast as they rise.

- Demand uncertainty: the DOE projection is a wide range (6.7% to 12%), and the buildout could slow.

- Commodity risk: uranium and fuel names move with commodity cycles.

- Policy and permitting: nuclear and power projects face regulatory and permitting risk.

- Leverage: trading the theme on margin amplifies both gains and losses, and you can lose more than you deposit.

Trading AI-energy stocks involves substantial risk, and most day traders lose money. Nothing here is a recommendation to trade any stock or the theme, and this article does not take a view on whether these stocks will rise or fall. Trading a fast-moving theme differs from long-term investing; our guide to investing vs trading covers the distinction.

What traders track (signals, not stocks)

Rather than a list of stocks, active traders track the signals that drive the theme: data-center power deals, the producers’ earnings and guidance, SMR project milestones, uranium prices, and the DOE and utility demand data. These are factual watch-items, not recommendations.

- Power deals: new data-center power-purchase agreements with producers.

- Producer earnings: results and guidance from the profitable generators.

- Developer milestones: licensing and project progress at the SMR names.

- Fuel prices: the uranium cycle behind the fuel names.

- Demand data: DOE, EIA, and utility figures on data-center electricity use.

Watching signals rather than chasing tickers is how traders follow the theme without treating any single name as a recommendation. You can trade US equities and ETFs across the complex through CMEG; the platforms and products available are described on the site, and all trading carries risk.

Frequently asked questions

What is the AI-energy trade?

It is the group of stocks tied to powering AI data centers: nuclear and gas power producers, power-equipment makers, small modular reactor developers, and uranium suppliers. They are watched as one theme because they all depend on rising data-center electricity demand.

Why is AI driving power and nuclear stocks?

Data centers are a large and growing source of electricity demand. The U.S. Department of Energy projects data centers could use 6.7% to 12% of US electricity by 2028, up from about 4.4% in 2023, which has pulled power and nuclear names into the AI theme.

What are SMR stocks?

SMR stands for small modular reactor. SMR developers such as Oklo, NuScale, and Nano Nuclear are building next-generation reactors and are pre-revenue, so they are more speculative and volatile than established, profitable power producers.

Which AI-energy companies report earnings and when?

This season GE Vernova reports July 22, Constellation Energy July 30, Cameco July 31, and Vistra, Talen, and NuScale on August 5, with Oklo on August 10. Dates change, so confirm before each event.

Are nuclear stocks a good investment?

This article does not give investment advice or recommend any stock. It maps the complex and its risks, including the large difference between profitable producers and pre-revenue developers. Whether any name suits a given trader depends on their own goals and risk tolerance.

What is a power-purchase agreement?

A PPA is a long-term contract in which a large buyer, such as a technology company, agrees to purchase electricity from a producer. These deals give producers revenue visibility and have become key catalysts in the AI-energy trade.

References

[1] U.S. Department of Energy, “DOE Releases New Report Evaluating Increase in Electricity Demand from Data Centers” (prepared by Lawrence Berkeley National Laboratory): data centers used about 4.4% of US electricity in 2023 (about 176 TWh) and are projected to use approximately 6.7% to 12% by 2028. https://www.energy.gov/articles/doe-releases-new-report-evaluating-increase-electricity-demand-data-centers

[2] Lawrence Berkeley National Laboratory, “Berkeley Lab Report Evaluates Increase in Electricity Demand from Data Centers,” January 2025. https://newscenter.lbl.gov

[3] Finnhub, company earnings calendar (report dates and consensus EPS estimates), retrieved July 3, 2026. https://finnhub.io

[4] CNBC, coverage of GE Vernova and the AI power boom, early July 2026. https://www.cnbc.com

[5] Federal Reserve Bank of St. Louis (FRED), Cboe Volatility Index: VIX (VIXCLS), value for July 1, 2026. https://fred.stlouisfed.org/series/VIXCLS

Disclosures: Trading involves substantial risk and is not suitable for every investor. Capital is at risk and most day traders lose money. Leverage amplifies both gains and losses, and you can lose more than you deposit. Client accounts are not SIPC or FSCS insured. This content is provided for information and education only. It is not investment advice or a recommendation of any security, strategy, or account type, and it does not take a view on whether any stock or theme will rise or fall. Company names are shown only as factual members of the AI-energy complex and are not recommendations; pre-revenue developers carry particularly high risk. Electricity-demand figures are from the U.S. Department of Energy and Lawrence Berkeley National Laboratory, company estimates from Finnhub, and market context from CNBC and FRED, as dated above. See our full disclosures and policies.